One aspect of watching for any signs of monetary system change is to monitor various markets. Most the time markets tends to operate under established norms that can provide some insight into whether anything unusual is happening. If markets stray from established norms for an extended period of time, it becomes reasonable to wonder if this may mean the current financial and monetary system is under abnormal stress.

Let's discuss a couple of examples looking at where markets seem to be what we might describe as confused.

---------------------------------------------------------------------------------------------------------------------

An Inverted Yield Curve

Typically, long term interest carry a higher yield than short term interest rates and only rarely do we see this "invert" such that shorter term rates actually go higher than longer term rates. Just this year, we have seen this condition arise at times. Certainly, the spread between longer term rates and shorter term rates has stayed somewhat reduced for an extended period of time even when not inverted. Historically, when this situation occurs, many analysts predict that a recession will follow an inverted yield curve.

But these days, there seems to be a lot of conflicting opinion on all this. Some do take the traditional view that an inverted yield curve means we will see a recession coming in the US. Others say that the current situation is different and the yield curve is only inverted because the US Fed is refusing to lower short term rates in the face of declining world wide rates and that money seeking yield is pouring into US bonds.

At this time, there seems to be a lot conflicting signals in these markets leading us to call them confused. On the one hand, we hear much of the mainstream financial media assure us that no recession is forthcoming and the US Fed is also taking this view. On the other hand, the Fed has sharply reversed its course since late last year and has started into a program of lowering short term rates (and ending their QT program) despite saying they see no signs of recession at this time. Then we have President Trump also touting the economy as "the greatest in history" even while he says the Fed must lower rates further because everyone else has lowered their rates and the US is at a competitive disadvantage. Of course we understand that their are 2020 election political ramifications to what happens with interest rates. But for now, markets seem unsure of whether to conclude the US economy is strong and healthy or needs more easy monetary policy to avoid heading into recession. The political atmosphere in the US contributes to the confusion.

Rising Gold and a Rising US Dollar

Normally, gold and the US dollar tend to have an inverse relationship meaning that when the US dollar is strong, it tends to depress gold prices stated in US dollars. However, in 2019 we are seeing another unusual market condition where BOTH the US dollar and gold prices stated in US dollars are strong over the last several months. There are all kinds of explanations out there as to why this may be happening. I saw this one by Lobo Tiggre on Kitco which may as plausible as any I have seen (investor worry/fear is causing money to flow into perceived safe havens and for now both the US dollar and gold are viewed that way). So what are these markets telling us? That harder times are ahead? If so, why is the US stock market holding up reasonably well since it normally looks ahead like all markets do? Various economic indicators bounce up and down, but seem to stay mostly positive. Again, we seem to be getting mixed signals from markets that appear confused.

-------------------------------------------------------------------------------------------------------------------------

Conclusion: One theory as to why markets are behaving unusually is that so much attempted manipulation of markets has taken place over the last 10 years that traditional normal market behavior has been distorted. Central banks all over the world have implemented easy monetary policies in response to the 2008 crisis. There are now trillions of dollars globally invested in bonds that pay a negative yield (the bond purchaser has to pay the bond issuer interest which is completely reversed from normal bond market conditions). The creation of various derivative products allows large market players (central banks, large multinational banks, large hedge funds, etc) to actually gain enough leverage in some markets to be able to manipulate the price direction for those markets, at least in the short term. Governments also engage in currency market manipulations when they feel it serves their purposes. On top of currency wars we have trade wars just as Jim Rickards accurately predicted several years ago (see Currency Wars - 2011).

Whatever is causing these confused markets, it appears that many traditional market norms can no longer be relied upon to try and forecast future trends. This suggests that market volatility and uncertainty for investors is likely to continue and even increase.

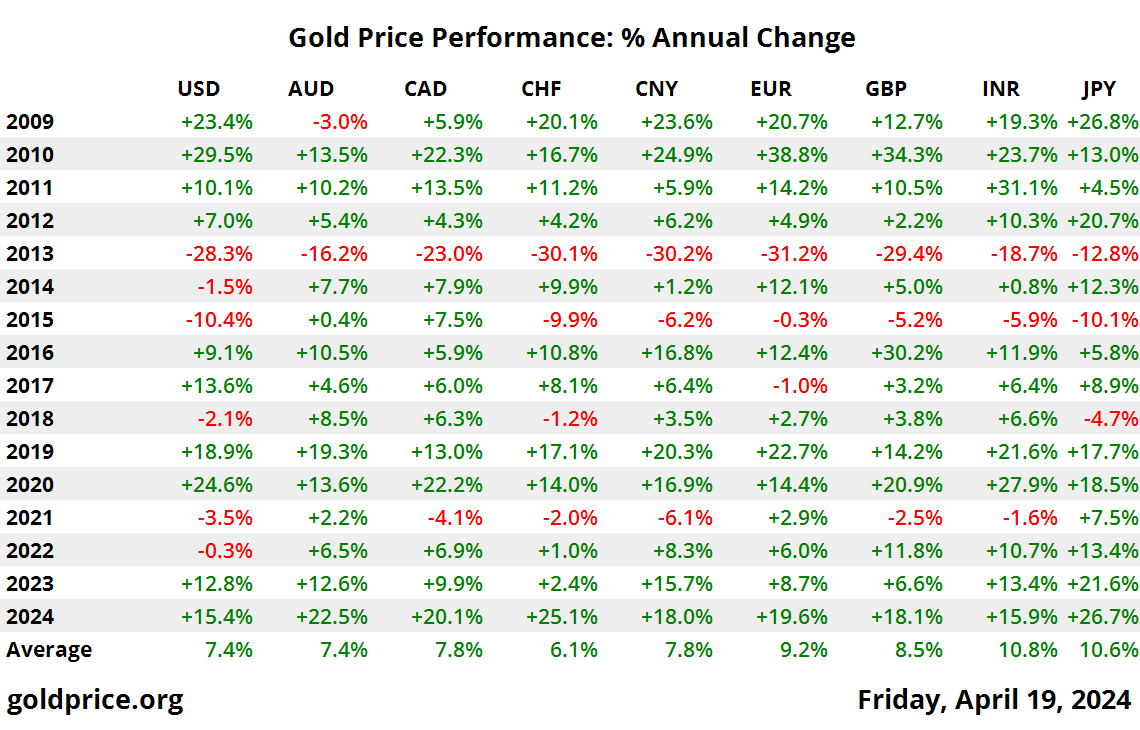

This could explain why gold has now reached all time highs in many major currencies around the world and seems to be heading that way in US dollars even as the US dollar itself remains relatively strong thus far. Click here to see how gold has fared against the major global currencies (average annual gain of 9-12% since 2004 with a huge surge across the board in 2019 averaging around 20%).

{kind=link}

Will any of this lead to some kind of major reform or reset of the present monetary system? Is it even possible to get the kind of political consensus needed to do some kind of major monetary system reform? Only time will tell us the answers. That is what this blog attempts to monitor. There are many ideas for potential system reform as we have noted here. But there seems to be very little political consensus around any one idea at this time.

No comments:

Post a Comment